Comment

Sustainability and ESG in the built environment: What 2026 has in store

Now the dust has settled on a busy start to the year, our Sustainability and ESG team share their reflections on what's coming in the world of Sustainability and ESG in 2026 and why it matters for real estate and the built environment. From major updates to building standards, through to significant shifts in corporate reporting, this year is set to bring meaningful change across the sector.

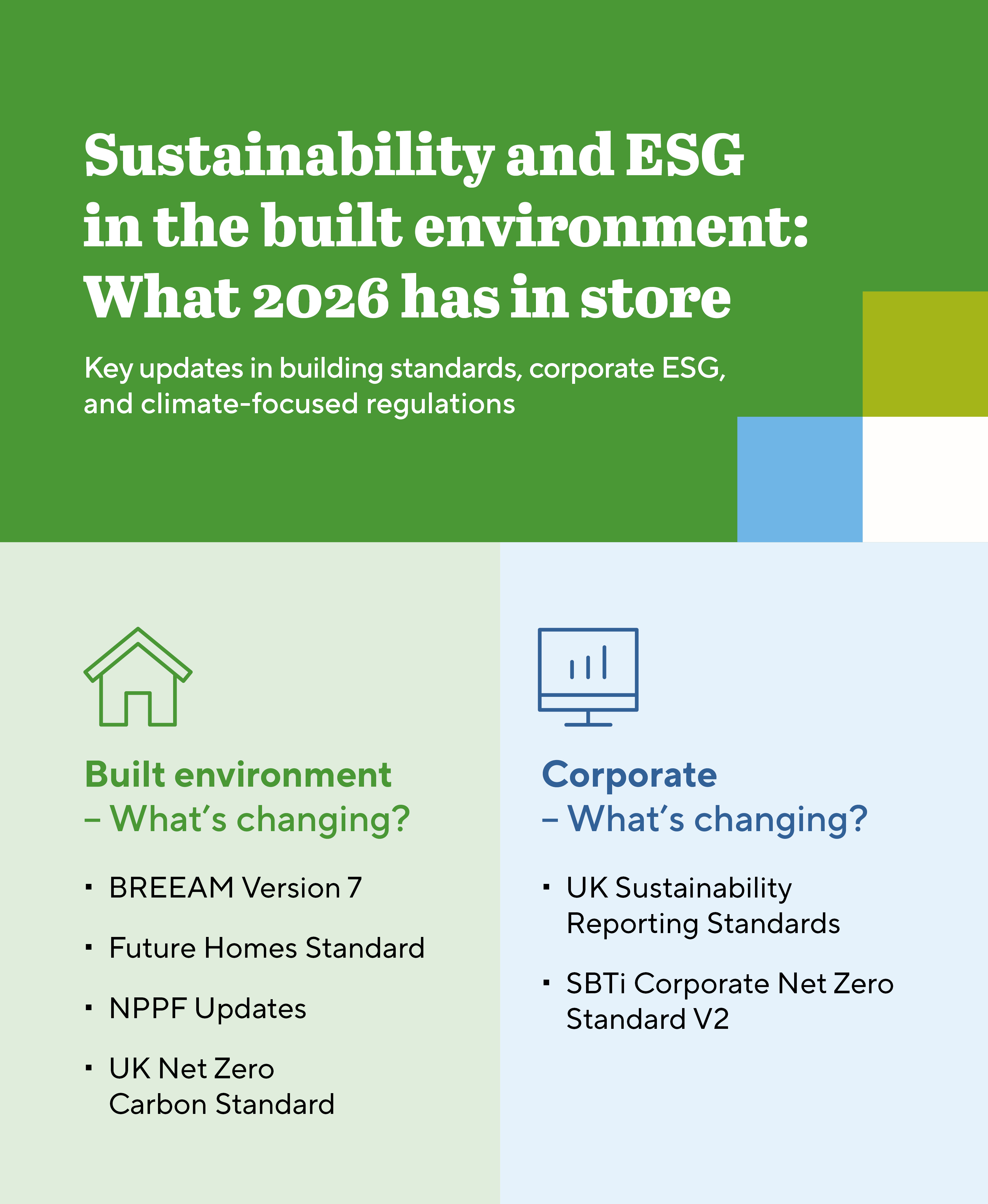

Changes that will affect the built environment

BREEAM Version 7

With BREEAM V6.1 now closed, attention has turned to V7 which represents a substantial overhaul with major changes in most sections, introducing new credits and updates to methodology.

We are looking forward to seeing how the industry responds to new credits around flexible demand response and smart energy systems. These changes offer an opportunity to close the performance gap and move away from some of the more 'tick-box' exercises.

Achieving higher ratings such as Excellent and Outstanding are likely to become more challenging under the new version. However, we see this as a positive step forward and look forward to working with our clients to navigate the changes.

The Future Homes Standard (FHS)

After years of waiting, we are expecting the Government to finally publish the FHS, which will require homes to achieve a c.75% carbon reduction beyond the requirements of the Part L 2013 Building Regulations. We expect to see electric heating systems and solar PV mandated.

National Planning Policy Framework (NPPF)

The NPPF consultation in December aims to better address climate change, providing further guidance on mitigation and adaptation measures. There are also proposed amendments to the Planning and Energy Act 2008 to restrict the ability of local plans to set higher energy efficiency standards for residential development.

UK Net Zero Carbon Building Standard (NZCBS) Version 1

Following feedback on the Pilot Version of the UKNZCBS, we look forward to the full release expected this spring. Major changes are expected to include the introduction of clearer delineation between building owners and tenants, and a 'Practical Completion On-Track' checkpoint, allowing speculative buildings to demonstrate progress and assess performance against the standard at building completion. We have been actively involved in the development of the standard and would be pleased to share our insights once it is released.

What to watch out for in corporate reporting

UK Sustainability Reporting Standards (UK SRS)

The UK SRS are the UK Government’s emerging framework for corporate sustainability and climate related disclosures, designed to create consistent, transparent and comparable ESG reporting across UK companies. The UK SRS are currently in the final consultation and endorsement phase, with final standards expected to be published in early 2026. The Financial Conduct Authority has recently released a consultation on changes to the Listing Rules and has proposed mandatory climate disclosures from 2027, except for Scope 3 emissions, for which it is 'comply or explain' from 2028-related disclosures, designed to create consistent, transparent and comparable ESG reporting across UK companies.

SBTi Corporate Net Zero Standard v2

The SBTi is developing Version 2 of its Corporate Net-Zero Standard which aims to be science-based, innovative and practical following feedback from businesses. Whilst the standard is expected to be published in 2026; companies may continue to set new targets under the current Corporate Net-Zero Standard (V1.3) and Near-Term Criteria (V5.3) until 31 December 2027.

2026 is shaping up to be a pivotal year for sustainability across the built environment, and we will continue to monitor developments closely. To discuss what this could mean for your projects, please contact our team:

Built environment:

Fiona Lomas-Holt

Paul White

Corporate:

Snigdha Jain

23 February 2026

Key contacts